The survey of 702 employers shows a major rebound in the job market remains a way off.

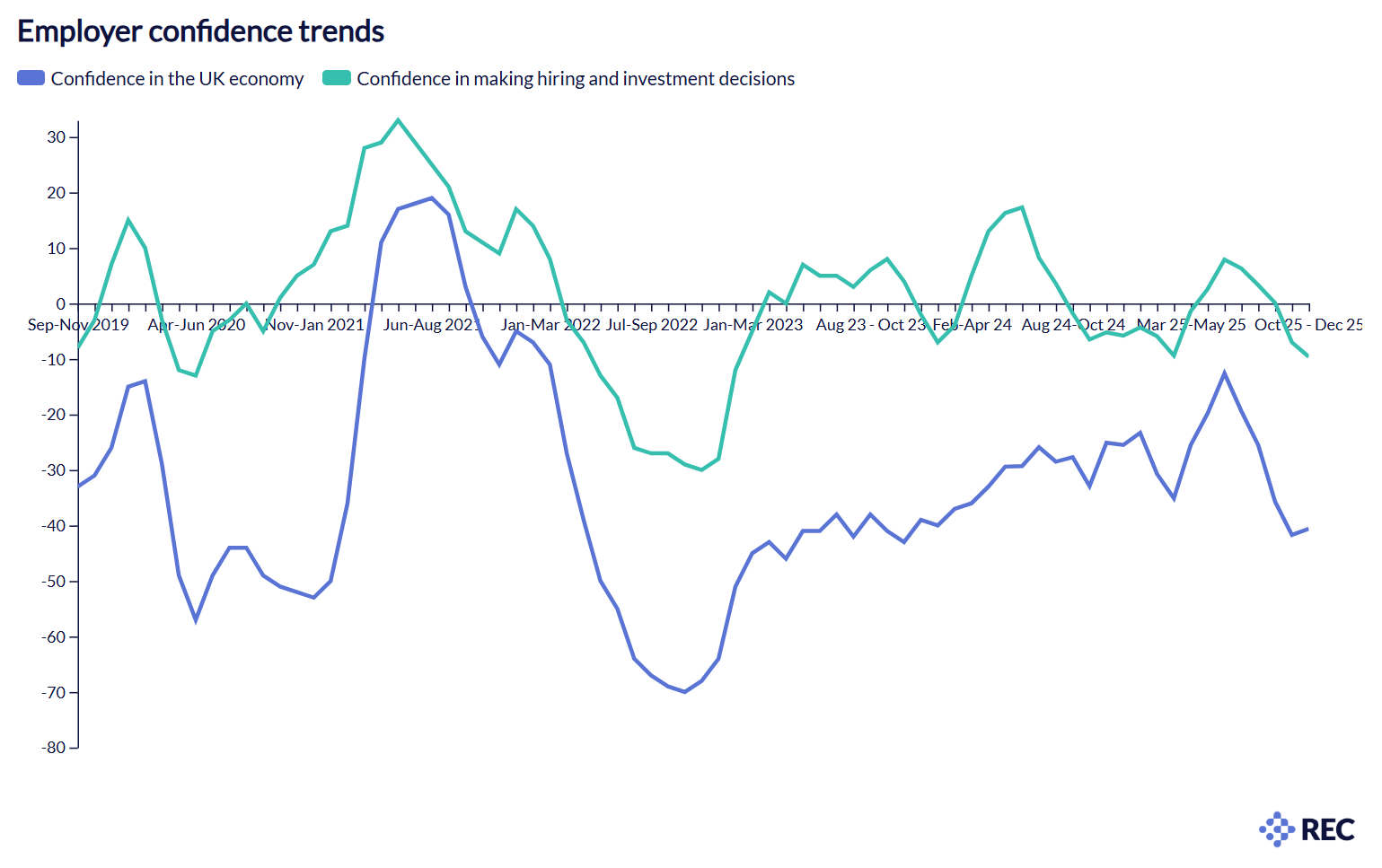

Surveyed employers’ confidence in the UK economy weakened further between October and December 2025. Perceptions of economic conditions fell by five percentage points from the previous quarter to net: -41%, driven by particularly low sentiment in October. Confidence did improve a little after the Chancellor’s Autumn Budget in November and December.

In a further setback for the labour market, employers’ confidence in making investment and hiring decisions also slipped back into negative territory. It averaged net: -10% across October to December, which is the weakest level since spring 2025.

But the survey also contains some encouraging signs in the details of the findings.

Hiring intentions for the next three to nine months remain positive. Sentiment on both short‑term and medium‑term temporary hiring dipped slightly but stayed above zero, as did expectations for permanent hiring in both timeframes. This will offer some reassurance to the more than 1.8 million people aged 16 and over who are unemployed, after a tough 12 months for jobseekers.

Neil Carberry, REC Chief Executive, said:

“The volume of Budget speculation for a fiscal event only a few weeks before Christmas had a clear effect on employers’ view of the economy as a whole. It is no surprise, therefore that December was a little weaker. Despite this, overall hiring intentions remained positive and the real test is whether those intentions were put into action in January. So far, anecdote from recruiters suggests that this is starting to happen, but confidence is fragile. Sentiment can shift quickly. Underpinning business confidence should be at the heart of the government’s labour market strategy and that starts with much more pragmatism about the real costs of the Employment Rights Act to workers and companies.

“Government needs a policy punch strong enough to knock lingering negativity out of the picture. A Bank of England rate cut next week is unlikely and monetary policy cannot carry the load anyway. What is needed is a genuinely pro‑enterprise, pro‑investment agenda that puts muscle behind the industrial strategy, tackles high-cost pressures like energy and avoids tax rises that choke activity.

“December’s shift toward more practical unfair dismissal rules in the Employment Rights Act was a rare moment when common sense beat ideology and businesses have something to cheer. It should set the tone for the consultation period ahead, not stand as the exception.”

- Short-term permanent hiring sentiment remained positive but softened slightly. Over October–December, the net balance stood at +11%, two points lower than the previous quarter, though sentiment improved month-on-month from October to December. Optimism was strongest in the South outside London (net: +20%), while confidence was more subdued in London (net: +6%) and weakest in the Midlands (net: +4%). Larger and mid-sized employers remained more optimistic than smaller firms, and the gap between private sector employers (net: +14%) and the public sector (net: 0%) widened significantly.

- Medium-term permanent hiring expectations also eased, falling four points to net: +12%. As with the short-term outlook, sentiment was strongest in the South (net: +23%) and weakest in the Midlands (net: 0%) and London (net: +5%). Large and mid-sized employers continued to report stronger expectations than small organisations, while public sector confidence fell into negative territory.

- In the temporary and contract market, short-term hiring sentiment dipped slightly to net: +11%, with notable month-to-month volatility. Confidence declined in London (from net: +10% in August-October to net: +5%) and turned negative in the Midlands (net: -2%), while remaining strong in the South outside the capital (net: +21%).

- Medium-term temporary hiring sentiment also weakened modestly to net: +12%, with lower confidence among larger employers (from net +30% across June-August, through net: +18% in August-October, to net: +13% in October-December) and the public sector (from net: +14% to net: +8%) compared with previous quarters.