- One in eight (13%) workers say money worries hinder concentration

- Over a quarter (27%) of workers are at the tipping point financiallyThe number of workers reporting financial difficulties over the last 10 years has doubled

A new study entitled 'Working Well', from the Social Market Foundation think-tank conducted in partnership with financial employee benefits provider Neyber, finds that one in eight workers (13%) report that money worries have affected their ability to concentrate at work.

The study shows low financial resilience is a significant cause of stress across the UK workforce.

Katie Evans, SMF economist, the report's author, says:

“The UK’s workforce lacks financial resilience. It’s clearly affecting our ability to concentrate at work and blunting our productivity.

“This low financial resilience is a problem across industries – and it’s getting worse. The proportion of workers reporting that they face financial difficulties nearly doubled over the decade to 2013/14.

“These money worries have a clear impact on how people feel and behave as they go about their day-to-day lives and jobs.”

Key findings:

- Four in ten workers (40%) say money worries have made them feel stressed over the last year

- Over a quarter (27%) of workers are at the tipping point financially

- A quarter (25%) say they have lost sleep over money worries

- One in eight workers (13%) report that money worries have affected their ability to concentrate at work

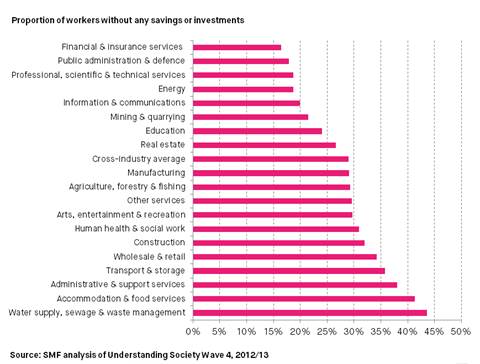

- Nearly 50% of workers (48%) are not putting any money aside for anything more than regular bills

Monica Kalia, co-founder of Neyber comments: “These findings should provide a wakeup call for UK employers because they clearly demonstrate how productivity is impacted by factors such as stress and anxiety, with both driven by financial worries. The fact that these issues are apparent across all sectors of the economy means that we have consistently failed to recognise some of the key drivers of poor productivity in the UK economy.

“For far too long politicians, policy makers and economists have chided Britain’s workforce for its failure to improve productivity without taking account of the wellbeing factors that can affect employees. This clearly has to change if we are to continue to emerge from the recession with a workforce that is fit to deliver economic growth at home and meet the competitive challenge in global markets.”

Surprisingly, workers in relatively well-paid industries also have low levels of savings and lack financial resilience.

The report suggests ways of tackling the problem:

Katie Evans, the author of 'Working Well', says: “Employers need to help their staff to learn healthy financial behaviours and build financial resilience. As poor financial resilience affects all income groups, the answer isn’t just higher levels of pay.

“Workplace pensions have already been introduced to build financial resilience later in life. One option is to extend auto-enrolment policies to include short-term savings or income protection insurance as well as pension savings. However, auto-enrolment programmes are difficult to design and take a long time to organise.

“New financial mutuals, providing affordable savings and credit products using bonds of trust between those in particular professions, could be one way of building a culture of financial resilience through the workplace.

“Tax incentives are already offered on some workplace savings and investment programmes, but only the largest employers are usually able to make these schemes available to their workforce. Extending these privileges to new workplace savings schemes would increase the number of workers who can benefit and maximise the number of households able to build financial resilience by saving through their payroll.

“Firms could also consider simple changes, like printing a recommended monthly savings goals on payslips or offering budgeting applications alongside online payroll to help improve the financial capability of their teams”.